How Can Marketing Leaders Manage Loyalty Point Liabilities in Regulated Environments?

Sign up for our newsletter for trending top content!

Introduction

Loyalty programmes create long-term customer value, but they also create financial obligations. Every point issued represents a future redemption commitment that must be measured, monitored, and accounted for appropriately. Under IFRS 15, organisations offering customer loyalty rewards generally recognise part of the transaction price as a contract liability until customers redeem points or the obligation expires. For banks, insurers, and fintech companies, this makes loyalty programme management as much a financial governance issue as a customer engagement strategy.

This guide explains why loyalty point liabilities matter in regulated industries, how financial institutions can balance customer engagement with financial control, the governance practices that support sustainable loyalty programmes, and how technology improves liability visibility and operational compliance.

Why Do Loyalty Point Liabilities Matter in Regulated Industries?

Every loyalty point issued represents a potential future cost. As customer participation increases, the value of outstanding points also grows, creating liabilities that organisations must monitor carefully. In regulated industries such as banking, insurance, and financial services, this requires close collaboration between marketing, finance, compliance, and risk management teams.

According to Deloitte, financial institutions increasingly rely on data-driven governance to strengthen operational resilience and customer trust. Loyalty programmes contribute to this objective only when organisations maintain accurate records of point issuance, redemption activity, expiry rules, and financial obligations.

Poor liability management can create several challenges:

- Inaccurate financial reporting.

- Unexpected redemption costs.

- Poor cash flow forecasting.

- Regulatory scrutiny.

- Customer dissatisfaction caused by inconsistent redemption policies.

- Limited visibility into programme performance.

Marketing Leaders should therefore understand that loyalty programmes influence both customer engagement and financial performance. A well-governed programme balances attractive rewards with responsible liability management, ensuring that commercial objectives remain aligned with financial controls.

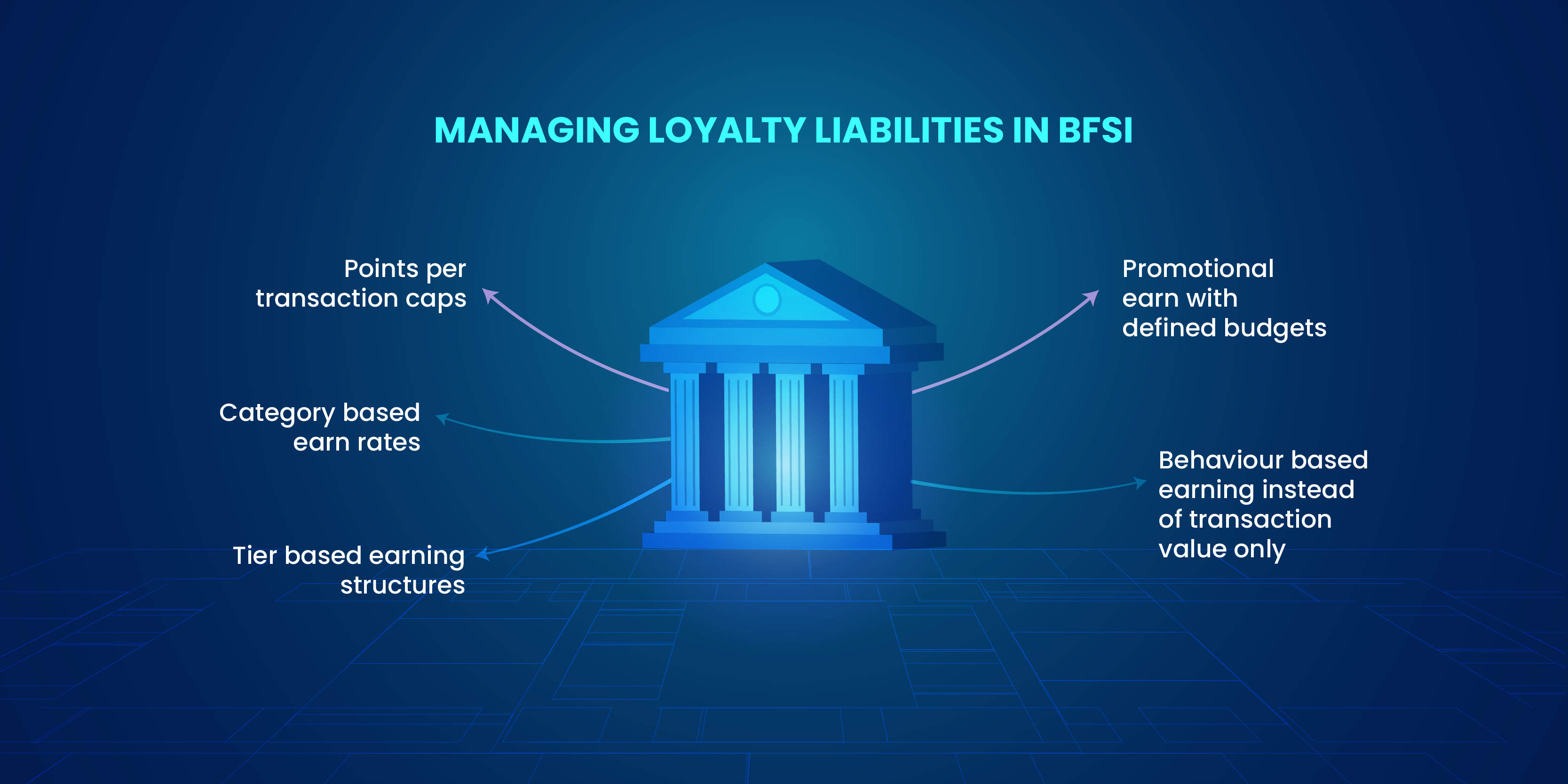

How Should Banks and Financial Institutions Manage Loyalty Point Liabilities?

Managing loyalty liabilities requires a structured operating model that combines financial governance with customer experience. Rather than monitoring redemption only at campaign level, organisations should track the entire loyalty lifecycle from point issuance to redemption or expiry.

A practical governance framework includes:

Under IFRS 15, organisations generally estimate expected redemptions and recognise revenue as performance obligations are satisfied. Accurate redemption forecasting therefore becomes essential for financial reporting.

Marketing Leaders should work closely with finance teams to understand how campaign design influences liability growth. Large promotional campaigns, accelerated earning opportunities, and extended validity periods may improve customer engagement but also increase future redemption obligations if not managed carefully.

Effective governance allows organisations to balance programme attractiveness with long-term financial sustainability.

What Governance Framework Supports Sustainable Loyalty Accounting?

Strong governance begins with clearly defined ownership. Marketing teams design customer engagement strategies, but finance, compliance, and operational teams all contribute to successful loyalty programme management.

A practical decision framework includes:

According to Forrester, customer trust depends on consistent experiences supported by transparent operational processes. Loyalty programmes should therefore communicate earning rules, redemption conditions, expiry dates, and programme changes clearly to participants.

Governance also extends to supplier management. Organisations should ensure fulfilment partners, reward providers, and technology platforms support reporting, security, and audit requirements appropriate for regulated industries.

The strongest loyalty programmes integrate financial control into programme design from the beginning rather than treating compliance as a separate operational activity. This approach reduces financial risk while supporting long-term customer engagement.

How Can Technology Improve Loyalty Liability Management?

Managing loyalty point liabilities manually becomes increasingly difficult as programmes grow. Marketing, finance, and compliance teams need accurate, real time visibility into point issuance, redemption, expiry, and outstanding liabilities to support both customer engagement and financial reporting.

According to McKinsey, organisations that digitise operational processes improve decision-making and reduce administrative complexity through better data visibility. Loyalty platforms deliver similar benefits by automating calculations, tracking customer activity, and providing centralised reporting.

A modern loyalty platform should support:

Technology also enables Marketing Leaders to analyse redemption trends and customer behaviour together, helping organisations balance commercial objectives with financial sustainability. Automated reporting reduces manual effort while giving finance teams greater confidence in liability calculations and programme performance.

How Does Rekyndl Support BFSI Loyalty Programmes?

Financial institutions require more than customer engagement tools. They need platforms that combine loyalty management, governance, reporting, and operational visibility within a secure environment.

Rekyndl helps organisations build and manage customer loyalty programmes while supporting structured governance and scalable operations. The platform combines customer segmentation, marketing automation, loyalty journeys, reward management, and reporting within one integrated ecosystem.

A typical loyalty workflow includes:

- Customer onboarding.

- Behaviour-based campaigns.

- Automated points allocation.

- Configurable earning and redemption rules.

- Redemption tracking.

- Campaign analytics.

- Liability reporting support.

- Integrated reward fulfilment.

Customers can redeem points across multiple categories, including gift cards from more than 5,000 brands, hotel bookings, flight bookings, dining vouchers, sports experiences, golf experiences, merchandise, bus bookings, concierge services, and curated experiences.

By combining automation with reporting and configurable programme rules, Rekyndl enables Marketing Leaders to improve customer engagement while maintaining greater visibility over programme performance and loyalty liabilities.

What Framework Should Marketing Leaders Use When Evaluating a Loyalty Platform?

Selecting a loyalty platform should involve both commercial and operational considerations. Marketing Leaders should evaluate whether the platform supports sustainable programme growth while providing the governance required in regulated industries.

A practical decision framework includes:

According to Bain & Company, long-term customer relationships generate greater commercial value than isolated transactions. Marketing Leaders should therefore prioritise platforms that balance financial control with customer engagement rather than focusing solely on campaign functionality.

The most effective loyalty platforms integrate analytics, governance, automation, and reward fulfilment to create programmes that remain commercially sustainable as customer participation grows.

Frequently Asked Questions

What is a loyalty point liability?

A loyalty point liability represents the future obligation created when customers earn points that can be redeemed for rewards. Until those points are redeemed or expire, organisations generally recognise a financial liability in accordance with applicable accounting standards such as IFRS 15.

How do banks account for unredeemed loyalty points?

Banks typically estimate the expected value of future redemptions and recognise a contract liability until customers redeem their points or the obligation expires. Actual accounting treatment depends on applicable accounting standards, programme design, and professional financial advice.

What is the breakage rate for banking loyalty programmes?

Breakage refers to the percentage of issued loyalty points that customers never redeem. The rate varies significantly between programmes depending on customer behaviour, expiry policies, reward relevance, and programme design. Organisations generally estimate breakage using historical redemption data and regularly review those assumptions.

Can Rekyndl support regulated loyalty programmes?

Yes. Rekyndl supports loyalty management through customer segmentation, marketing automation, configurable programme rules, reporting, and an integrated rewards ecosystem, helping financial institutions operate scalable loyalty programmes with stronger operational visibility.

When should organisations review loyalty point liabilities?

Finance and marketing teams should review loyalty liabilities regularly, particularly after major campaigns, financial reporting periods, or significant changes to programme rules. Continuous monitoring improves forecasting accuracy and supports stronger financial governance.

Conclusion

Managing loyalty point liabilities requires more than accurate accounting. Marketing Leaders must balance customer engagement, financial governance, operational visibility, and regulatory expectations throughout the loyalty lifecycle.

By combining structured governance with automation and analytics, organisations can create loyalty programmes that remain commercially sustainable while delivering meaningful customer experiences. As loyalty programmes become increasingly sophisticated, technology will play a central role in helping financial institutions manage liabilities with greater confidence and transparency.

Discover how Rekyndl for Financial Services and Fintech helps organisations build compliant loyalty programmes with marketing automation, configurable reward rules, reporting, and an integrated rewards ecosystem.

https://www.therewardstore.com/rekyndl/solutions/financial-services-fintech

Sign up for our newsletter for trending top content!